CECL Methodology – Vintage Analysis Application

The FASB’s guidance on the Current Expected Credit Loss (CECL) model is not prescriptive and allows for a number of methodologies to be used in order to fulfill the requirements. Vintage analysis is an allowance for loan lease losses (ALLL) calculation methodology that has been suggested as being the new minimum standard for CECL compliance. If you are interested in an introduction to Vintage Analysis before looking at how it’s applied, read CECL methodology – introduction to vintage analysis.

According to an Abrigo whitepaper, “The Basics of Vintage Analysis,” vintage analysis accounts for expected losses by allowing an institution to calculate the cumulative loss rates of a given loan pool and in so doing, to determine that loan pool’s lifetime expected loss experience. This includes a reasonable approximation of probable and estimable future losses gleaned by applying historical gross charge-off information to forward-looking qualitative and environmental factors.

Be better equipped to manage the ALLL under CECL; Prepare for CECL with defensible methodologies.

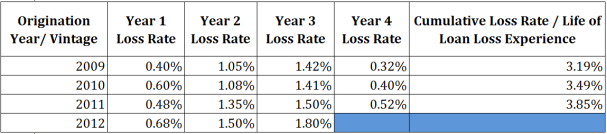

The table below illustrates the usefulness of vintage analysis as a forecasting tool. The example shows four, four-year loan pools separated into vintages and calculates the life-of-loan loss experience of each group in the cumulative loss rate column. This is done by dividing each year’s net charge-offs by the original principal balance (some may use original principal and interest, for simplicity, principal alone is used below). The respective vintage’s original principal balance remains the denominator in each annual calculation, as it references the specific vintage’s original balance. The loss experience of this original balance is tracked annually and summed over the life of the loan leaving a cumulative, life-of-loan loss rate based on historic averages. For loans originating in 2009, the total life-of-loan loss rate is 3.19% and the 2010 rate is 3.49%. The goal is to use the existing data to forecast future loss rates, denoted in the blue shaded sections of the chart.

In addition to life-of-loan loss data, primary drivers like macroeconomic indicators of qualitative factors can be added to the expected loss calculation to reach a forecast supported by both quantitative and qualitative data points. For example, by identifying the unemployment rate as a primary driver of changes in the international, national, regional and local conditions qualitative risk factor (Q factor), you can look for trends that correlate to historical loss experience. If an increase in the unemployment rate leads to an increase in charge-offs six months later, this information can be factored into forward-looking loss projections. Additionally, identifying correlations between different factors is similar to Q factor adjustments under the current, incurred loss framework.

The goal is to express the impact of changes in external factors while incorporating analysis of where the loan pool is in its loss history. In our example, life-of-loan loss experience shows that a forecasted increase in the unemployment rate, (taken from CBO or Treasury Department estimates, for example), will have a bigger impact on loans in their second and third years than on loans near maturity in year four.