How Are Your Peers Preparing for CECL?

As CECL is implemented, the allowance for loan and lease losses, or ALLL, is being called the allowance for credit losses, or ACL.

As financial institutions lay the groundwork for transitioning to the current expected credit loss model, or CECL, many are curious about how peers are preparing for CECL and where they are in tackling what’s considered the biggest accounting change in banking history.

After all, the FASB’s guidance on CECL is not prescriptive, and institutions have varying effective dates, so it can be helpful to understand the experience of other institutions in deciding whether to build their own models for estimating losses or select third-party vendors to help with modeling and implementation.

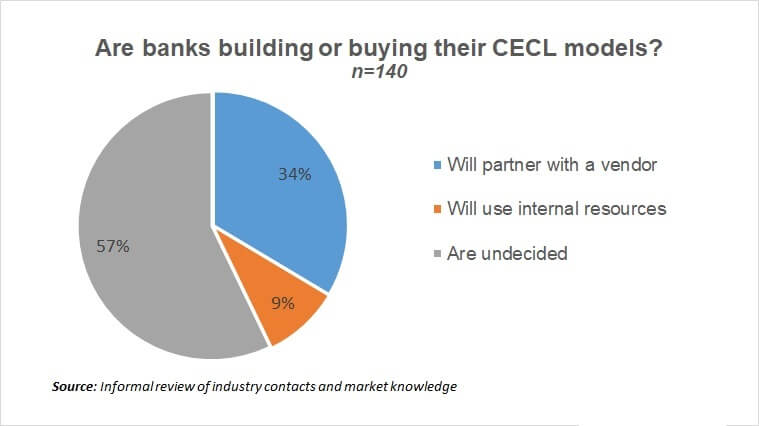

An informal review of CECL readiness at 140 larger community banks finds that more than half (57 percent) haven’t yet decided whether to buy or build CECL models. Approximately 60 of the banks have either decided to use internal resources to prepare for CECL or have selected a third party. The informal review was based on research among Sageworks contacts and market knowledge.

Learn more about navigating the CECL transition.

Tim McPeak, executive risk management consultant at Abrigo, said the banks in the review had assets between $5 billion and $30 billion.

“Approximately 60 of the banks we reviewed, or about 43 percent, have chosen a vendor or a plan for implementing CECL,” McPeak said. “Of those 60, 13 plan to develop a credit loss model internally and the remaining 47 are working with third parties.”

Of the 80 banks that have not yet made a decision on how to implement CECL, about 25 to 35 are actively evaluating options that include Abrigo, McPeak said.

“This is an interesting part of the market, because it includes larger community banks, including many that are subject to DFAST,” or Dodd-Frank Act Stress Testing, McPeak said. “And I think many of the banks we reviewed are SEC filers, so these banks have the closest deadline.”

Banks that file with the Securities and Exchange Commission must comply with CECL in 2020; all other financial institutions have until the following year. McPeak noted that financial institutions that are subject to stress testing under Dodd-Frank may already have a “deep bench” of personnel and resources for fairly sophisticated analysis in the credit risk area, so they have a higher propensity to utilize internal resources for CECL. “A lot of what DFAST asks is sophisticated and forward-looking credit models,” he said. “There is some CECL overlap, at least conceptually.”

“Work your process” for CECL preparation

For that reason, McPeak suspects a fair number of the banks that haven’t yet identified their implementation plans may end up using internal resources. In any case, he cautioned against assuming that banks aren’t doing anything to prepare for CECL if they haven’t yet made the build or buy decision.

“I’d be very surprised if the other banks that haven’t yet made a decision aren’t in the process of making one,” McPeak said. “Maybe they’re finishing an RFP or waiting on results. They may be doing some robust internal preparations, even if they haven’t settled on a plan. My advice to those that don’t yet have a plan is to work your process for making a decision. If you don’t have a process in place to figure out how you’re going to do this, you may need to reach out for help.”

In addition to FASB-imposed deadlines for financial institutions to adopt CECL, there are SEC requirements for disclosing in SEC filings the expected material effects of accounting changes, both financial impacts and impacts of other significant matters, such as planned changes in business practices for CECL or technical violations of debt covenant agreements resulting from CECL adoption.

McPeak noted that some SEC-registered institutions have already begun disclosing information about CECL’s impact. He expects the next round of 10-K filings with the SEC is likely to shed more light on whether institutions are using internal resources or a vendor to implement CECL, and the filings at that time may have more specifics on methodologies under consideration. “I’ve talked with some bankers about whether disclosing a range of adjustment resulting from CECL would be appropriate, but you’d need to have some parallel CECL calculations run through most of 2018 to be able to have a range for the 2018 10-K filing in March 2019,” he said.

“It’s not just the transition deadline that the clock is ticking on,” McPeak said.

Additional Resources

Whitepaper: CECL Solution Buyer’s Guide

Webinar: CECL: The Hidden Complexities to Simple Approaches for Community Institutions