CECL and IFRS 9: How Are They Different?

CECL implementation timelines have been altered since the release of this post. Find updated information here.

Financial institutions around the world are revising how they estimate credit losses, but institutions subject to the International Accounting Standards Board (IASB) standards have gotten a head start on those that will follow the U.S. Financial Accounting Standards Board’s current expected credit loss model, or CECL.

Earlier effective dates of IASB’s International Financial Reporting Standard (IFRS 9) aren’t the only substantive differences from CECL. Even though both standards incorporate forward-looking models for estimating credit losses of financial instruments, they have distinct differences of which both domestic and international institutions should be made aware.

In an article from KPMG’s IFRS 9 Institute, the authors discuss the different implementation challenges for domestic and foreign institutions while explaining the high level differences of the two standards.

Effective dates

IFRS 9 has already been in effect for over half a year. The standard was implemented by financial institutions with annual periods beginning on or after Jan. 1, 2018. CECL goes into effect for financial institutions with annual periods beginning after Dec. 15, 2019 for SEC filers and periods after Dec. 15, 2021 for non-public business entities (PBEs).

Challenges

U.S. financial institutions who are complying with IFRS 9 for their foreign operations may want to leverage some of their existing model work for CECL adoption. KPMG predicted in the article that “U.S. banks will consider IFRS 9’s requirements relative to their expected CECL decisions to limit undue organizational complexity and operational burden for foreign reporting purposes.”

Although the largest impact of CECL and IFRS 9 will be observed in bank and credit unions, alternative lenders may experience challenges given that they are often not regulated as heavily as banks. This means that if an alternative lender holds financial assets, they will most likely have to undergo a larger organizational shift to ensure that their models are compliant.

Learn more about navigating the CECL transition.

Measurement of expected credit losses

One of the primary differences discussed in the KPMG article was the projection of losses for financial instruments. CECL requires that all instruments are projected over the life of the loan. IFRS 9, however, varies its projection requirement based on whether an asset is classified as stage 1, 2 or 3.

According to BDO UK, stage 1 classification consists of assets where credit risk has not increased significantly since initial recognition, and stage 2 occurs when credit risk has increased. Stage 3 is when a financial asset is considered credit impaired. Assets classified as stage 1 only need to have their losses projected over 12 months. Assets classified as stage 2 and 3 are similar to CECL and have a life-of-the-loan requirement. Additionally, stage 3 assets should recognize interest income on a net basis.

Garver Moore, of Abrigo’s Advisory Services, said in a response about the two standards that, “A well-considered modeling regime for CECL can be readily varied by changing modeling assumptions to produce stage results under IASB’s IFRS 9 approach, but translation of stage 1 IFRS 9 results to the lifetime notion is a more difficult direction. Application of stage 2 modeling to stage 1 assets to produce a whole-portfolio lifetime loss expectation is theoretically straightforward, but implementation approaches many not be operationally scalable.”

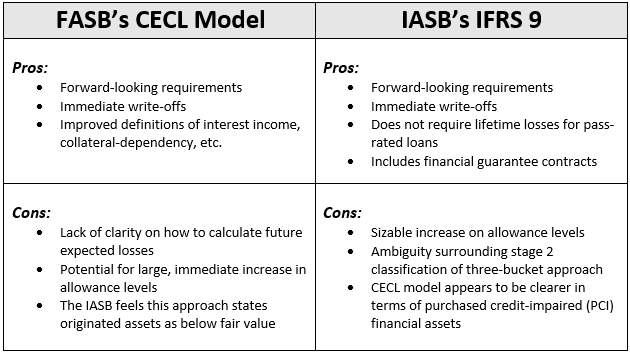

Potential pros and cons of both models:

Source: ALLL.com

“In our field experience, we have found the impact to capital concerns under CECL to be exaggerated, at least under present economic outlooks. A large part of this stems from the banking industry’s tendency to over-reserve under an ‘incurred’ notion through use of post-hoc adjustment. Credit unions and non-depository institutions may find the impact more severe. However, CECL gives institutions extremely broad latitude in presenting investors with a good faith estimate of lifetime credit loss exposure, taking into account reasonable expectations about the future, while the IASB standard at least offers more prescriptive guidance on classification and treatment within those classifications,” said Moore.

Whether institutions have already implemented IFRS 9 and are preparing for CECL, or if they only need to comply with one of the two models, there are solutions available to assist in making and sustaining practical transitions.

Whitepaper: Practical CECL Case Study: Hidden Complexities

Webinar: Best Practices for Running and Validating a CECL Model